TERRA TECH CORP.

2040 Main Street, Suite 225

Irvine, California 92614

(855) 447-6967

www.terratechcorp.com

December 18, 2017

VIA EDGAR TRANSMISSION

Mr. Kevin J. Kuhar

Accounting Branch Chief

Office of Electronics and Machinery

United States Securities and Exchange Commission

Division of Corporate Finance – Mail Stop 3030

Washington, DC 20549

|

|

Re: |

Terra Tech Corp. |

|

|

Form 10-K for the Fiscal Year Ended December 31, 2016 Filed March 31, 2017 Form 10-Q for the Quarterly Period Ended June 30, 2017 Filed August 8, 2017 File No. 000-54258 |

Dear Mr. Kuhar:

Terra Tech Corp., a Nevada corporation (the “Company,” “we,” “us,” or “our”), is submitting this letter in response to the comment letter from the staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”) dated September 29, 2017 (the “Comment Letter”), with respect to the Company's Annual Report on Form 10-K for its fiscal year ended December 31, 2015, filed with the Commission on March 31, 2017 (the “2016 10-K”); and the Company's Quarterly Report on Form 10-Q for its quarterly period ended June 30, 2017, filed with the Commission on August 8, 2017.

This letter sets forth the comments of the Staff in the Comment Letter and, following each comment, our response.

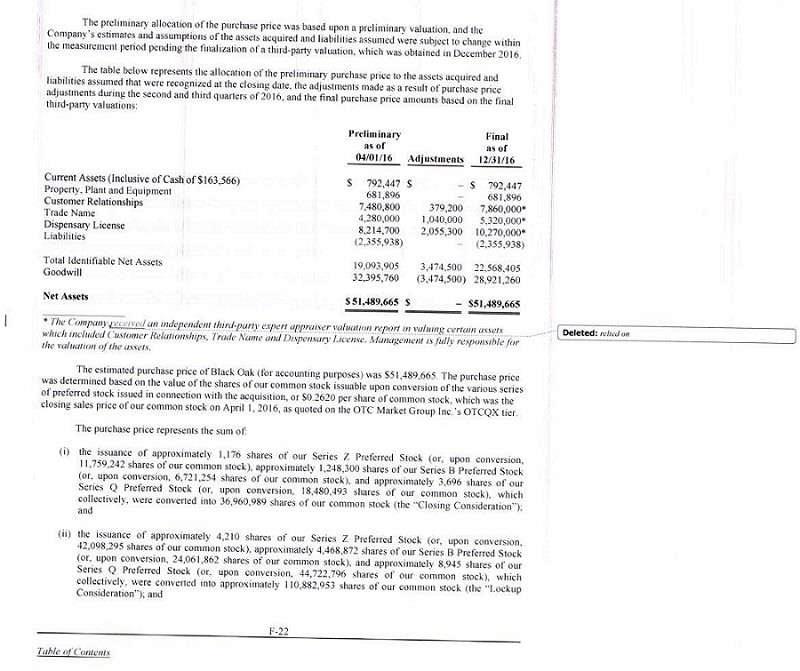

Black Oak Gallery, page F-22

4. We note your disclosure that the purchase price amounts are based on the final third-party valuations. Please revise future filings, including the requested amendment, to clarify the nature and extent of the third-party appraiser´s involvement and management´s reliance on the work of the independent appraisers. Also, refer to Question 141.02 of the Compliance and Disclosure Interpretations on Securities Act Sections which discusses your responsibilities should this filing be incorporated by reference into a Securities Act registration statement.

Response:

The Company respectfully acknowledges the staff’s comment.

The Company will adjust the disclosure in the footnote to the second table of Note 4 on page F-22 to read as follows:

“The Company received an independent third-party expert appraiser valuation report in valuing certain assets which included Customer Relationships, Trade Name and Dispensary License. Management is fully responsible for the valuation of the assets.”

| 1 |

We acknowledge that:

|

|

· |

the Company is responsible for the adequacy and accuracy of the disclosure in the filing; |

|

|

· |

staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the filing; and |

|

|

· |

the Company may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States. |

Should there be any questions that might be facilitated by contemporaneous dialogue, please feel free to call our general counsel, Joseph Segilia at (646) 258-7567, or me at (855) 447-6967.

Thank you for your ongoing courtesy in this matter.

Sincerely,

|

By: |

/s/ Michael C. James |

|

|

Michael C. James |

||

|

Chief Financial Officer |

| 2 |

|

3 |